|

AUTHOR: Bernard Laurendeau, Managing Partner at Laurendeau & Associates Brain drain in Sub Saharan Africa Brain Drain is a severe problem in low- and middle-income countries and particularly acute in Sub-Saharan Africa. In its 2016 World Economic Outlook[1], the IMF noted that the “outflow of skilled labor and young people seeking better educational opportunities outside the continent’s borders will continue rising, and the trend is worrying”. Impact of brain drain: gap in expertise The impact of brain drain is significant on emerging countries economies. For a country like Ethiopia, the impact can be measured in actual numbers, on GDP and job creation. In the public sector, deals are not optimally negotiated with multinationals- looking to grab opportunities that the opening of certain markets bring like that of telco- directly impacting the government coffers. Policies remain frozen in time making it difficult to attract investors, and hence putting a brake on job creation. In the private sector, diversity and maturity of products offered by banks remains low, decreasing the volume of transactions and overall money velocity in the country. Value chains are inefficient, not integrated, leading to high overhead and high prices for consumers. Startups seldom turn into scaleups as they have a hard time attracting talent that can unleash their power, making it difficult to lead to market-creating innovations[2] in economies that so badly need it. Therefore, expertise in all sectors is crucial for a country like Ethiopia to successfully transition to a middle-income country. Expert secondments sponsored by international development institutions are necessary, with the caveat that they should be temporary otherwise they create an artificial secondary talent market, but not sufficient. Emerging economies require expertise at scale. Reversing the brain drain: a digital brain gain Working remotely was trending before covid-19 burst into our lives. But if there is one positive aspect that the pandemic brought about, it is that lesson that remote work is here to stay. So why not leverage this trend to reverse the brain drain? In January every year, most Ethiopians living abroad come back to Ethiopia and, between visits to family members and touristic escapades, they explore ways to professionally engage with their home country. But after the January honeymoon, romance fizzles in February and disappears by March. Remote engagement can ensure that the romance sustains in February and remains strong until December. But remote work is not enough for the romance to sustain. Most of these engagements are usually built on a foundation of patriotism. Unfortunately, for many, patriotism should be the reason one should feel obliged to offer their expertise on a pro bono basis. Pro bono is not sustainable and usually leads to ill-defined and blurry engagements. Hence, the second ingredient necessary for that romance to sustain is: compensation. Indeed, experts need to be compensated for their brain capital. Filling the expertise gap through a curated expert network There are many experts and very highly skilled professionals who want to engage with their home country regularly. This expertise needs to be curated and linked strategically with clients who need it, and at the right time. A country like Ethiopia is growing rapidly, albeit some challenges. Liberalization of many sectors is expected. Hence, the country needs now more than ever subject-matter expertise in many fields (e.g., private equity, corporate restructuring, international arbitration, digital transformation, investment banking, fund management, talent development, cybersecurity, PR, smart city etc.) and in all verticals (e.g., Agriculture, Health, Medical Devices, Tech, FMCG, Aviation, Telecom, Transportation, etc.). Curated expert networks can reverse the brain drain, ensure a brain gain through digital means, while delivering expertise at scale to emerging economies growing rapidly.

0 Comments

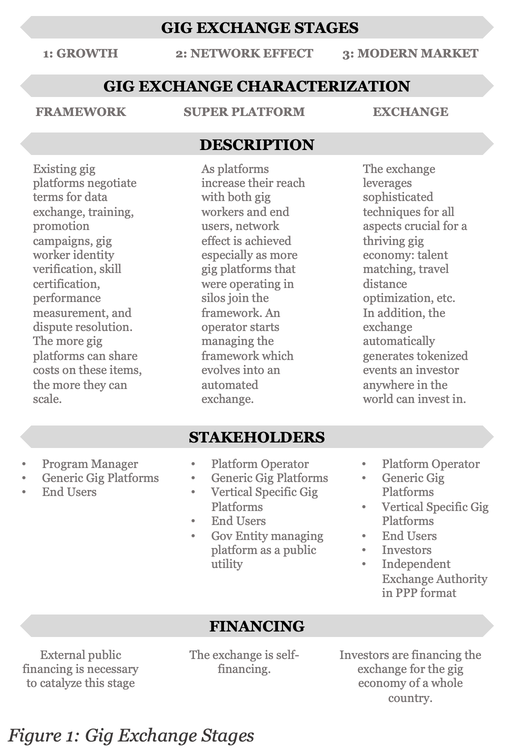

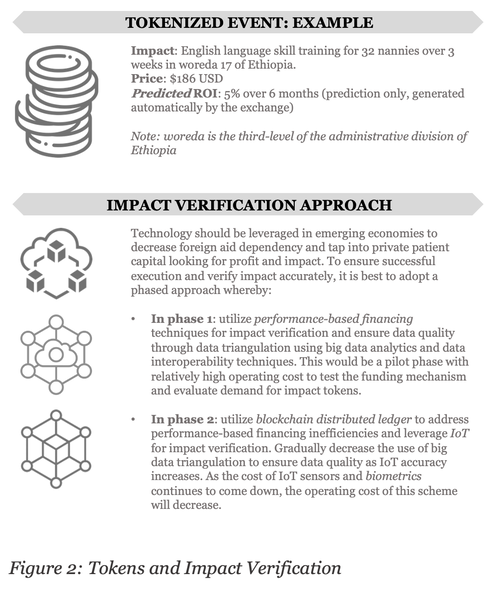

AUTHOR: Bernard Laurendeau (Managing Partner, Laurendeau & Associates) Current State of the Gig Economy in East Africa An assessment[1] issued by Mastercard in 2020 showed that Kenya, with a population of a bit over 50 million, had 5 million gig workers. The report further showed that 80% of gig workers accessed gigs through mobile and 60% of them joined a digital platform in the last 2 years. With Ethiopia’s youthful population quickly reaching 115 million, informal gig workers exist in the millions. Although digital platforms for gig work are only recently emerging, there is a great potential for them to scale to create millions of decent jobs in the next few years. However, these platforms should not scale in silos. They should come together to accommodate the future of work where gig workers who have different skills want to make themselves available in a way where they control their schedule and decide how far they want to travel to deliver their services. In other words, in a country like Ethiopia, a female gig worker should be able to provide rides on ZayRide from 8 to 11am after she drops her kids at school in the morning, then become a nanny from 11:30am until 1:30pm on Gooday, tutor students from 2 to 3:30pm using Astegni before she picks up her kids from school at 4pm, then spend her late evening designing graphics for a client she found through FreelanceEthiopia. Enters the Exchange In the future, a gig worker should be able to seamlessly sell their services from one centralized platform. What would such a centralized platform look like? Look no further than stock markets. According to Wingham Rowan, “when new technologies for information retrieval, dissecting data, payment transfers, graphic displays, and back-office processes emerged, financial institutions built themselves markets that come as close as possible to perfectly frictionless. A trader at Goldman Sachs or Citi uses software that seamlessly identifies and executes opportunities across multiple exchanges, forces down overheads, and minimizes transaction risk while proactively combing for openings to suit current objectives.”[2] If a trader or investor can have access to such sophisticated platforms, doesn’t a gig worker deserve a sophisticated labor market too? With very complex labor laws and legacy systems, it might be difficult for western countries to implement such exchanges. The situation is different for emerging economies. These countries can indeed leapfrog and become trend setters by designing and implementing bespoke labor exchanges. The Stages of Implementation Each country has its own idiosyncrasies; thus, it is important to customize the exchange to local laws and design it based on the capabilities of local gig platforms. Nevertheless, the maturity stages of implementation remain the same for any emerging economy (See figure 1).  Ultimately, in its mature stage, the Gig Exchange for the gig economy of a whole country is financed by investors. Like the stock market, investors can win or lose when they invest in impact tokens (See figure 2).  The case of Ethiopia

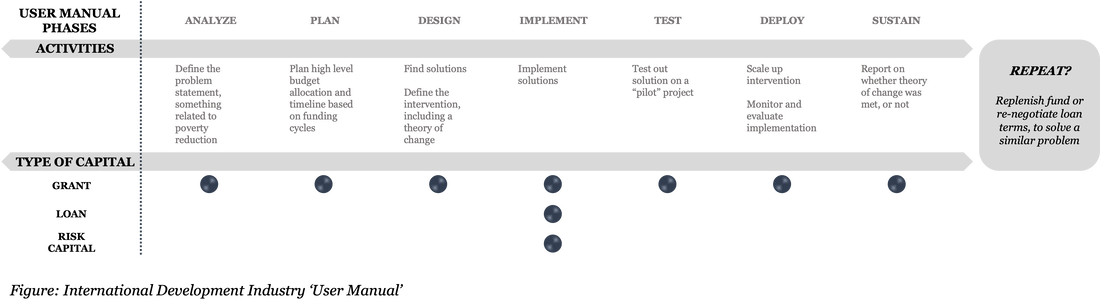

L&A has brought existing generic gig platforms in Ethiopia (Gooday, Taskmoby, ShegaMuya, PickPro, Gigs Ethiopia, Fetan, etc.) together into an alliance so that a Stage 1 framework as described above can be initiated. More platforms focused on delivery, taxi hailing or logistics (i.e verticals) can be brought into the fold to create a larger framework (i.e horizontally) breaking the silos while allowing each platform to thrive and scale. The framework would then incrementally grow into a super-platform and ultimately into an exchange. Ethiopia: setting a trend on top of following In June 2021 the Federal Parliament of Ethiopia approved and enacted a capital markets proclamation[3]. A Capital Market Authority and the Ethiopian Securities Exchange will become operational in 2022 with public-private partnership arrangements. The coming of a capital market in Ethiopia is of utmost importance not only for large corporations, but also for startups (including that in the Gig Economy) that have the potential to go IPO in a few years, creating an exit opportunity for investors. However, this has been a long time coming. Where Ethiopia could truly trailblaze and become a trendsetter would be with the establishment of the EGX, an innovative and disruptive way for finally cracking the tough nut of job creation. In Ethiopia, 2 million individuals enter the labor market each year hence the economy needs to create close to 8 thousand jobs every business day; A ticking time bomb that can be defused by the EGX. [1] Mastercard, September 2020, The Gig Economy In East Africa, https://newsroom.mastercard.com/mea/files/2020/09/The-Gig-Economy-in-East-Africa-White-Paper.pdf [2] Wingham Rowan, June 2021, Remaking the Modern Market, https://americancompass.org/essays/remaking-the-modern-market/ [3] Addis Fortune, June 2021, Stock Exchange to be operational through PPP, https://addisfortune.news/stock-exchange-to-be-operational-through-ppp/ AUTHOR: Bernard Laurendeau (Managing Partner, Laurendeau & Associates) At the heart of most International Development efforts is the noble goal of reducing poverty, although it is often coupled with geopolitical interests. Since the 1970’s, trillions of dollars have been poured into International Development interventions, flowing from the West into what was then called the third world, now referred to as frontier or emerging economies. After a few decades in action, the trillion-dollar development industry[1] has yielded limited results in alleviating poverty in southern hemisphere nations. In the meantime, a nation like South Korea lifted itself out of poverty through industrialization and innovation- instead of external assistance - grew to become the 10th largest economy in the world and transformed into a significant donor. If the development industry could be likened to a piece of software, it would require a major upgrade to address all the bugs and issues accumulated over the years. But before considering a ‘product’ upgrade, let us examine the current user manual of this industry. It is rather straight forward – see figure below.  At first glance, the user manual seems comprehensive, efficient, and effective. However, when performing a more thorough troubleshooting of the industry, what emerges as the root cause of all its bugs and issues is the operating system itself. Indeed, the underlying premise of the industry is that poverty exists in many forms around the world, and it needs to be reduced. Case in point: as a young engineering student in France, I remember organizing fundraising events to build a kindergarten in Ethiopia. A few years later, after I graduated and stopped raising funds, the kindergarten budget started running dry. The playground equipment was not maintained, some teachers were not getting paid on time; in short, what we had built was not sustainable. To alleviate the “poverty” in education, we forced the construction of a kindergarten. Instead, we should have approached this problem by finding a solution to create “wealth”, obviously for the kids in the of form of knowledge, but also for the whole ecosystem serving them. Indeed, the solution could have been to invest in an entrepreneur with a sustainable model, able to raise funds and resources to build an innovative kindergarten. Similarly, for large international development interventions, addressing poverty by poverty reduction interventions yields limited result. Instead, these interventions should be planned and designed as wealth creation programs. Such programs would create self-sustaining ecosystems that are bound to yield greater results. There are positive signals in the development industry indicating that it is headed in that direction. It is reflected in the program taxonomy (e.g. catalytic) as well as in the type of funding deployed recently (e.g. risk capital). It also reflected in the evolution of the type of assistance; Between 2000 and 2017, Development Finance Institutions (DFI’s) contributions have increased seven-fold from US$12 billion to US$87 billion when development assistance only tripled, going from US$54 billion to US$146 billion during the same period[2]. These signals are encouraging however they seem to be only minor upgrades. To create real and sustainable impact in emerging economies in a short amount of time, the industry requires a major upgrade, a paradigm shift. In essence, there needs to be a Disruption of International Development for Good (DIG4Good). For good because it remains a noble cause. Also, because the industry should cease to exist for good after a set amount of time when all problems are solved in a sustainable manner. A key recipe for success in the new paradigm is the ownership of the disruption journey. Indeed, the disruption journey needs to be owned by recipient countries in collaboration with partners. Rephrasing the latter sentence in the new paradigm, the disruption journey needs to be owned by investee countries in collaboration with stakeholders. Decision makers from investee countries should define a tailored, localized, and agile DID4Good Playbook- rather than a static user manual- to create wealth within a timebound roadmap, to progressively sunset all external assistance while ensuring local market dynamics take over. In the second part of this paper, we will dive deeper into the specific aspects of the DID4Good Playbook. [1] Developing countries face $2.5 trillion annual investment gap in key sustainable development sectors, UNCTAD Report, Geneva, Switzerland, 24 June 2014 [2] The Role of Development Finance Institutions in Enabling the Technology Revolution, Center for Strategic and International Studies (CSIS), June 17, 2019 Based on Bernard Laurendeau's Conversation with Nahoko Toyota - GM at Innovation Dojo Japan, GM at Kobe Global Mentorship Program and Startup Hub

After the lost decade of the 1990’s in Japan, the number of temporary workers dramatically increased due to the economic stagnation. The shift in the labor workforce, which was historically dominated by large corporations, led to a change in mindset. In the late 2000’s, a startup ecosystem started emerging in Japan. How has the mindset or startup culture evolved since then? Is the ecosystem growing? What proactive measures were taken to build the ecosystem? How are entrepreneurs fundraising? What does talent availability look like in this nascent ecosystem? We examine all these questions in our conversation with Nahoko Toyota. A Timid Startup Culture In general, the Japanese society is risk averse. However, when really looking hard at facts "in Japan the risk mainly exists in our minds" says Nahoko, “the worst thing that can happen for a young entrepreneur is for the startup to fail but there is always a social security system and companies hire candidates with entrepreneurial skills” she adds. Indeed, their livelihood or whole career success is not at stake, unlike in some developing countries. The Japanese society has traditionally been based on equality and uniformity; people still tend to hesitate to 'stand out'. Many top university students envision and aspire for a career in the government, as public servants, or working for large conglomerates also known as Zaibatsu’s, almost never for a small startup or as an entrepreneur. This limited aspiration to work for startups is not a surprise because startups receive limited attention in the media and entertainment and "when you cannot see it, you cannot be it" according to Nahoko. However, there seems to be a shift in career aspirations in the last decade or so. Increasingly, large companies have a Corporate Venture Capital (CVC) arm- usually structured as a separate entity- and intrapreneurship is encouraged. Many individuals who have gained experience in startup ecosystems abroad are integrated in large companies or startups in Japan and playing the role of 'interpreter' or 'intermediary', translating novel and disruptive approaches into the existing corporate or governmental environment, including highly regulated industries. Startup funding Access to finance has greatly improved and is less of an issue for growing startups in Japan.

In addition, in the early stages entrepreneurs have access to Government led incubators and accelerators managed by private firms (e.g., Deloitte[1], 500Startups[2]) and staffed with individuals with experience in the private sector. For example, 'Innovation Officers' in Kobe city are contract-based public servants with experience working in the private sector. Startup Regulatory Environment Japanese startup entrepreneurs tend not to challenge the current laws and regulations but to find a way to co-exist with them while creating a better user experience. The policies and regulatory environment leave whitespaces for entrepreneurship and innovation. Disruption in the Japanese startup ecosystem can be qualified as "harmonious" as there is a close linkage or symbiosis between the industry and the startup ecosystem (e.g. Docomo Ventures[3]). Incentives and interests are aligned between startupers, corporations, and policy makers which usually leads to little friction between all those ecosystem actors. In addition, CxO's from scaling startups are starting to serve the ecosystem as angel investors and mentors for the next generation of startupers. Clusters are also formed to build innovation ecosystems like the Kansai (Kyoto-Osaka-Kobe) Startup Ecosystem[4]. Finding talent Local talent is increasingly aware of the startup industry and interested in joining it although this has not become mainstream yet. There have been nationwide campaigns like J-Startup[5] to entice the youth to join the ecosystem and grow globally. Interestingly, a popular TV show from South Korea called startup[6] seems to have captured the attention of the youth and is democratizing the concept of startups as well. Furthermore, attracting talent from abroad remains an option through the startup visa coordinated by the Ministry of Economy, Trade, and Industry (METI)[7] but coordinated at the municipality or city level. Taking stock The Startup ecosystem in Japan is growing in its volume and breadth of disruption; “It is also developing its own uniqueness in comparison with over ten years ago when people were looking at Silicon Valley and pondering how to copy and paste it” says Nahoko. Global standards and best practices have been incorporated into the startup ecosystem. According to Nahoko, “now that we learned what needs to be localized in the local context, I believe we are in a much better place to start, support, and invest in startups in Japan.” [1] Tokyo Acceleration Program, Operating the Aoyama Startup Acceleration Center supported by the Tokyo Metropolitan Government, Deloitte, September 15, 2015 [2] 500 Startups Kobe Accelerator 500kobe.com & ecosystems.500.co/accelerate_aichi/growth_program [3] NTT DOCOMO Ventures, https://www.nttdocomo-v.com/en/ [4] Turning the Kyoto-Osaka-Kobe Bay Area into a Global Startup Ecosystem, Jetro, May 25, 2021 [5] https://www.j-startup.go.jp/en/ [6] https://asianwiki.com/Start-Up_(Korean_Drama) [7] https://www.meti.go.jp/english/policy/economy/startup_nbp/startup_visa.html AUTHOR: Feven Dagnachew (Senior Manager, Laurendeau & Associates)

መግቢያ ኢትዮጵያ በፈጣን ኢኮኖሚያዊ ፣ ማህበራዊና ፖለቲካዊ ለውጦች ላይ እንደመገኘቷ ፣ ዲጂታል ቴክኖሎጂ ለዓለም እያበረከተ ያለውን ከፍተኛ አስተዋፅዖ እየተመለከቱ በዝምታ ማለፍ አዋጭ አይሆንም ፡፡ ምንም እንኳን ከዚህ በፊት ስለ ዲጂታል ቴክኖሎጂ አስፈላጊነት የሚያስሱ ብሔራዊ ፖሊሲዎች ቢኖሩም አብዛኛዎቹ ለዋናው ስራ ሂደት (core business) ቅድሚያ ከመስጠት ይልቅ አስቻይ ለሆኑት መሰረተ ልማቶች ከፍተኛ ትኩረት የሰጡ ነበሩ፡፡ ዲጂታል ትራንሰፎርሜሽን ማለት አሰራርን በዲጂታል ቴክኖሎጂ ማገዝ መቻል ሲሆን አሠራርን ከማዘመነን በዘለለ ቀልጣፋና ወጪ ቆጣቢ መሆኑ ለፈጣን እድገት ምቹ ያደርገዋል:: በመሆኑም እ.ኤ.አ ከ2020 እስከ 2024 ዓ.ም በአጠቃላይ 7.8ትሪሊዮን የአሜሪካ ዶላር ቀጥተኛ ኢንቨስትመንት ይኖረዋል ተብሎ ይገመታል። [1] የዲጂታል ትራንስፎርሜሽን ስትራቴጂ 2020 እስከ 2025 በአሁኑ ወቅት የኢትዮጵያ መንግስት ተግባራዊ እያረገ ያለው የኢኮኖሚ ማሻሻያ የተለያዩ የፖሊሲ እና የስትራቴጂ መሳሪያዎችን እያስተዋወቀ እና ተግባራዊ እያደረገ ነው፡፡ ከነዚህም ፖሊሲዎችና ስትራቴጂዎች መካከል እ.ኤ.አ. ከ 2020 እስከ 2025 ባለው ጊዜ ውስጥ ተግባራዊ የሚደረገው ብሄራዊ የዲጂታል ትራንስፎርሜሽን ስትራቴጂ አንዱ ነው፡፡ ይህም የዲጂታል ትራንስፎርሜሽን ስትራቴጂ በአገሪቱ አስተማማኝ እና ውጤታማ አዳዲስ የስራ እድሎች መፍጠር ፣ ድህነትን ለመቅረፍ የሚችል እድገትን ለማስፋፋት እና አዳዲስ ዲጂታል ቴክኖሎጅዎችን በመጠቀም የመወዳደር አቅምን ለማሳደግ ያለመ ነው፡፡ ስትራቴጂው ከብሄራዊ ሶሺዮኢኮኖሚክ እና እድገት እቅዶች ከሆኑት ከብሄራዊ የ10 ዓመት የልማት እቅድና እና የሀገር በቀል የኢኮኖሚ ማሻሻያ አጀንዳ ላይ መሰረት ያደረገ ነው፡፡ በተመሳሰይ ሁኔታ ስትራቴጂው ከአህጉሩ የዲጂታል ትራንስፎርሜሽን ስትራቴጂ እና ከተባበሩት መንግስታት ከዘላቂ የልማት ግቦች እንዲሁም ከተለያዩ የአለም አቀፍ ኢኒሼቲቮች ጋር የተጣጣመ ነው፡፡ ለፈጠራ ምቹ ሁኔታን ለመፍጠር መንግስት የወደፊቱ እና የመፃሂ በቴክኖሎጂዎች ምርምርና ስርፀት ላይ በቁርጠኝነት መዋለንዋይ ፈሰስ በማድረግ ላይ ይገኛል፡፡ የዲጂታል ትራንስፎርሜሽን ኢኒሼቲቭስ አገሪቱ እየተጓዘችበት ያለውን የዲጂታል ትራንስፎርሜሽን መንገድ በመከተል አዳዲስ ተነሳሽነቶች ተግባራዊ እየተደረጉ ይገኛሉ፡፡ ከነዚህ ኢኒሼቲቮች መካከል በዋናነት የሚጠቀሰው ላለፉት ጥቂት አስርት ዓመታት በመንግስት ተይዞ የነበረውን የቴሌኮሙኒኬሽን አገልግሎት ነፃ ማድረግ ነው፡፡ የቴሌኮሙኒኬሽን ዘርፉን ነፃ ማድረግ ስፍር ቁጥር የሌላቸውን ዕድሎች እና ጠቀሜታዎች ይሰጣል፡፡ ከነዚህም መካከል ተወዳዳሪ እና ጥራት ያለው የቴሌኮሙዩኒኬሽን አገልግሎቶችን ለተጠቃሚዎች ከመስጠት ባሻገር በማደግ ላይ ባለው የኢትዮጵያ የቴሌኮሙኒኬሽን ዘርፍ ውስጥ ልምዱ እና አቅሙ ያላቸው ዓለም አቀፍ ኦፕሬተሮች ተሳትፎ የሞባይል ባንክ አገልግሎት ለማስፋፋትና ለማጠናከር እንዲሁም አገሪቱ ወደ ዲጂታል ትራንስፎርሜሽን የምታደርገውን ጉዞ ለማፋጠን ከፍተኛ አስተዋፅዖ ያበረክታል፡፡ በተመሳሳይ ሁኔታ የዲጂታል ክፍያ ስትራቴጂ መጀመር፣ የአርቴፊሻል ኢንተለጀንስ ኢንስቲትዩት መቋቋም፣ የዲጂታል ክህሎት ሀገራዊ የድርጊት መርሃ ግብር፣ ብሄራዊ የዲጂታል መታወቂያ እና ሌሎች በመንግስት እየተወሰዱ ከሚገኙ የዲጂታል ትራንስፎርሜሽን እንቅስቃሴዎች መካከል ይጠቀሳሉ፡፡ [2] ተጓዳኝ እድሎች አገልግሎት ሰጪ የሆኑ የመንግስት ተቋማት አሰራራቸውን ዲጂታላይዝ በማድረግ እና ኢንተርኔትን መሰረት ያደረገ የመንግስት (e-government) አሰራር ስርዓት ተግባራዊ በማድረጋቸው በወረቀት ላይ የተመሰረቱ የስራ ፍሰቶች ወደ ዲጂታል ማህደሮች መቀየር ፣ አገልግሎቶች በተጨማሪ በበይነመረብ መድረኮች መስጠት የሚችሉበትን አቅም ይፈጥርላቸዋል፡፡ ይህም የሀገር ውስጥ የሶፍትዌር ልማት በከፍተኛ ሁኔታ እንዲያድግ ከፍተኛ ሚና ይጫወታል፡፡ ከዚህ በተጓዳኝ የኢንኩቤሽን ማዕከላት፣ የስታርት አፕ ፐሮግራሞች፣ የስታርት ሃፕ ፈንዶች እና የኢኖቬሽን ከባቢ በከፍተኛ ሁኔታ እንዲያድግ እና እንዲጎለብት ያደርጋል፡፡ [3] የዲጂታል ክፍያው የኢ-ኮሜርስ ዘርፉን በሀገር አቀፍ ደረጃ በማስተዋወቅ እና በማስፋፋት ረገድ የማይተካ ሚና ይኖረዋል፡፡ ለሀገራዊ የኢኮኖሚ እድገቱ ቅድሚያ የሚሰጣቸው እንደ ግብርና እና ቱሪዝም ያሉ ዘርፎች ከፍተኛ ድጋፍ ያገኛሉ፡፡ እነዚህን ሁሉ የዲጂታል ለውጦች ተከትሎ የድርጅት ሃርድዌር፣ ሶፍትዌሮች እና ኢንፎርሜሽን ቴክኖሎጂን መሰረት ያደረጉ መፍትሄዎች ፍላጎት በከፍተኛ ሁኔታ ይጨምራል፡፡ በተመሳሳይ መልኩም ለአከባቢው ደንቦች እና ለደንበኛ ባህሪ የሚስማሙ መፍትሄዎች ፍላጎት ይጨምራል፡፡ ዲጂታል ኢኮኖሚው የመረጃ ማከማቻ እና የመከላከያ መገልገያዎች ወይም መሰረተ ልማቶች፣ ንግድ ለንግድ (B2B) መፍትሄዎችን ፣ የጥራት ማረጋገጫ ስርዓቶችን ወዘተ ይፈልጋል፡፡ ምክረ ሀሳባች

ማጣቀሻ [1] Digital transformation spending worldwide 2017-2024, Kimberly Mlitz , Jul 28, 2021 [2] Home-grown Economic Reform Agenda Progress Highlight 2012EC, Federal Democratic Republic of Ethiopia - Ministry of Finance, June 2021 [3] Digital Ethiopia 2025: A Strategy for Ethiopia’s Inclusive Prosperity, Federal Democratic Republic of Ethiopia - Ministry of Innovation and Technology, June 2020 [4] Barack Obama to name a “Chief Technology Officer”, VentureBeat, Matt Marshall, November 13, 2007 Brief Note on Ethiopia's Digital Payments Strategy from the National Bank of Ethiopia (NBE)7/30/2021 Ethiopia's Digital Payments Strategy (EDPS) was approved by the Council of Ministers on June 23rd, 2021. The Vision EDPS proposes is to 'Build a secure, competitive, efficient, innovative, and responsible payments ecosystem to support a cash-lite and financially inclusive economy'. It includes 4 strategic pillars and 32 actions. At an event organized by the FDRE Ministry of Innovation and Technology on July 24th 2021 to assess progress on the implementation of the Digital Strategy 2025, ato Solomon Desta - Vice Governor of the National Bank of Ethiopia and responsible for Financial Institutions Supervision - stated that "the 32 actions will be completed in the next 3 years". The Vice Governor further stated that the NBE has drafted a National Financial Inclusion Strategy to complement the EDPS, an effort led by the National Financial Council chaired by H.E MoFED Minister Ahmed Shide. With internet penetration increasing every year in Ethiopia, Medium, Small and Large Businesses are increasingly adopting digital marketing and digital payment solutions (QR code, contactless payments, cryptocurrencies and biometrics). With the telecommunication sector privatization and liberalization, internet penetration might reach upwards of 90% in the next 5 years. It is therefore important to ensure that digital payments are inclusive of all sectors and layers of society while making all transactions secure. Millions in Ethiopia are still unbanked and financially excluded hence digital payments constitute an opportunity for all to obtain access to formal financial and digital services. The approval of the EDPS is timely as it will constitute an essential addition to the portfolio of policies recently issued in view of digitizing Ethiopia. AUTHOR: Bernard Laurendeau (Managing Partner, Laurendeau & Associates), Samson Assefa (Partner, Swaye Ventures)

After a decade of steady growth, the entrepreneurial ecosystem in Ethiopia is open to catalytic funding. Ethiopia’s Economic Context As the fastest growing economy in East Africa, Ethiopia is poised to continue its growth trajectory supported by several factors. There is a young population (median age of 18) entering the workforce with close to 200,000 STEM students graduating each year, there are positive trends in poverty reduction since 2011, and there is a nascent but fast developing private sector and financial sector. In addition, there are regulatory tailwinds and strategic plans including the Home-Grown Economic Reform Agenda, Job Creation Strategy, Digital Transformation Strategy, the Start-Up and Innovative Businesses Proclamation soon to be approved, and the privatization of key State-Owned Enterprises (especially in the Telecommunication Sector). Ethiopian Entrepreneurship Ecosystem Over the last decade, the Entrepreneurship Ecosystem in Ethiopia has seen an organic growth of startups evolving in all sectors. Indeed, startups are seen flourishing in fintech, healthtech, job placement/gigs, cleantech, logistics, e-commerce, agritech, edtech, media & leisure, govtech, etc. In addition, the presence of support hubs such as incubators, accelerators, and co-working spaces is increasing. Government entities are also investing resources in the ecosystem with assistance from development partners. However, Ethiopia with currently 9 active technology hubs still lags behind compared to other African countries: 80 technology hubs were counted in South Africa, 85 in Nigeria, 56 in Egypt and 48 in Kenya in 2019[1]. One of the main challenges the ecosystem is facing is the gap in financing. Financing Gap Currently, Ethiopia’s value chain for start-ups and SMEs growth is fragmented. In the early stages of a startup lifecycle, many development partners are increasingly providing support through technical assistance and direct grants. In the growth stages, financing is fundamentally needed for successful development of startups. Ethiopian banks such as the Commercial Bank of Ethiopia (CBE) and Development Bank of Ethiopia (DBE) can provide finance to start-ups but require 30% matching and collateral. When it comes to Venture Capital (VC) and Private Equity (PE) financing, very limited capital is available. Ethiopia ranks 109 out of 125 countries in the VC and PE Attractiveness Index[2]. Across Sub-Saharan Africa, PE accounted for less than 10% of the 51 disclosed deals[3]. Kenya had the largest share of the reported deals followed by Uganda, Tanzania, and Ethiopia for the period between 2014 – 2019[4]. For established scaleups and innovative businesses, some can have access to bank loans and VC/PE capital, but transactions have been very limited as well. Therefore, despite the current abundance of liquidity supporting early-stage entrepreneurs both through financial and technical resources in Ethiopia, research conducted by the Ethiopian Jobs Creation Commission in partnership with private firms clearly underscores a lack of support structure, financial and technical, post the incubation phase of start-ups in the nation. Indeed, entrepreneurs are left to fall off a cliff post incubation programs. The Need for a Continuum of Capital A continuum of capital is needed to support entrepreneurs and fund an ample talent pool of youth and women entrepreneurs. The type of capital deployed is a critical ingredient for the growth of the ecosystem and needs to be carefully calibrated. A blended finance approach seems to be the most appropriate for the Ethiopian ecosystem:

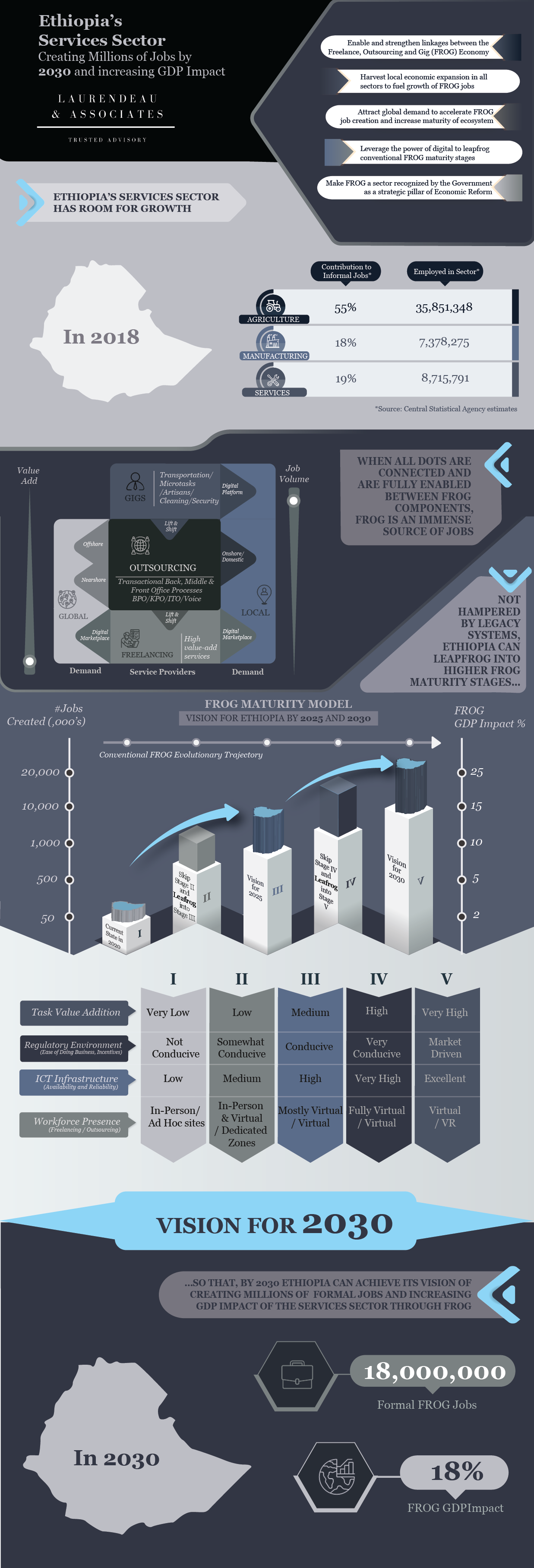

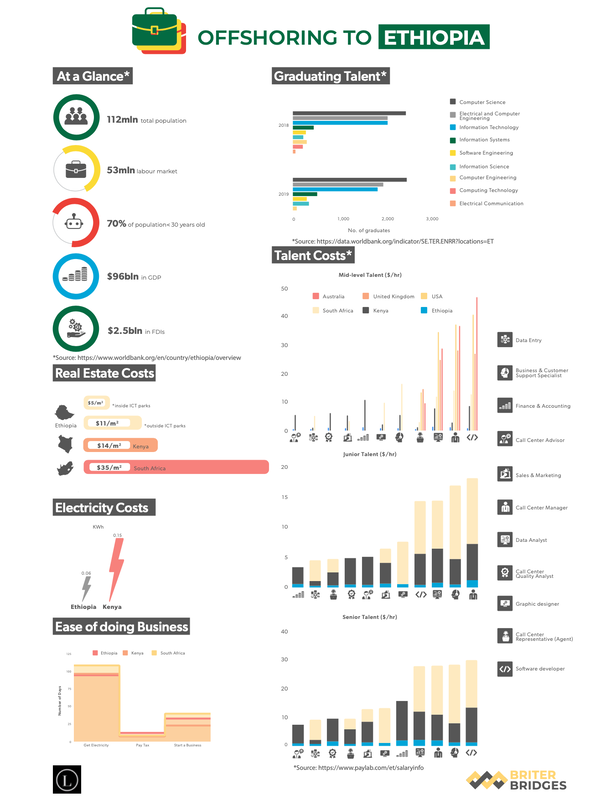

The amount of the blended finance is to be carefully estimated so as to not flood the ecosystem with too much capital, hence encouraging entrepreneurs to adopt unhealthy behaviors at loggerheads with growth and accountability. In addition, it is critical that the fund be managed by a professional fund management team from the private sector that has the experience to identify investments and work closely with Ethiopian entrepreneurs, youth and women, with full knowledge of idiosyncrasies of the ecosystem. Outlook Once such type of fund is deployed into the ecosystem, it is expected that more funds (Venture Capital, Private Equity, and Corporate Venture Capital) will be enticed to set up shop in Ethiopia, raising funds in hard or local currency, or a hybrid of both. This will ensure sustainability in the flow of capital in the ecosystem while lifting it up in the process, and also reducing future dependency from grant funding. [1] GSMA, Briter Bridges 2019 [2] Groh, Liechtenstein, Lieser , & Biesinger, 2018 [3] Asoko Insight, 2019 [4] AVCA; Ernst & Young, 2018 AUTHOR: Bernard Laurendeau (Managing Partner, Laurendeau & Associates) The nature of work is rapidly evolving around the world, primarily driven by the spread of technology and digital platforms. Ethiopia’s Informal Sector Ethiopia’s Services Sector has room for growth. Indeed, in 2018 close to 36 million were employed in the agriculture sector which contributed to 55% of informal jobs, over 7 million were employed in the manufacturing sector which contributed to 18% of informal jobs, and only around 8 million were employed in the sector sector which contributed to 19% of informal jobs[1]. In addition, if jobs in the informal sector can be given the recognition they deserve and defined using new job standards such as freelancer and gig, millions of formal dignifying jobs can be created in the next few years, especially if supported by digital. The Jobs Creation Commission recognizes informal employment and the gig economy as a crucial mode of employment for millions of citizens and that it should be supported with proper policy directives. In Kenya, 5 million gig jobs were created in 2020, where 80% of gig workers accessed gigs through mobile and 60% joined digital platforms in the last two years[2]. This example from Kenya- half the population of Ethiopia- not only illustrates the volume of jobs digital platforms can bring up to the surface but also the speed at which it can penetrate the workforce, if done in an inclusive way. Millions in Ethiopia are still unbanked and financially excluded hence digital payments constitute an opportunity for all to obtain access to formal financial and digital services. Digital Payments With internet penetration increasing every year in Ethiopia, Medium, Small and Large Businesses are increasingly adopting digital marketing and digital payment solutions (QR code, contactless payments, cryptocurrencies and biometrics). With the telecommunication sector privatization and liberalization, internet penetration might reach upwards of 90% in the next 5 years. It is therefore important to ensure that digital payments are inclusive of all sectors and layers of society, while making all transactions secure. The Ethiopian Digital Payment Strategy approved in June 2021 constitutes an essential addition to the portfolio of policies recently issued in view of digitizing Ethiopia and ensuring an inclusive ecosystem. The FROG economy in Ethiopia There is a growing list of private sector actors providing services directly or indirectly related to Freelancing and Gigs especially through digital means. A taskforce was formed at the JCC to assemble the most established players in the FROG economy, to place FROG at the core of Ethiopia's Services sector transformation. Indeed, FROG has the potential to accelerate job creation and add significant value to Ethiopia’s economy. By coming together as a unified team, taskforce members are identifying linkages between Freelancing, Outsourcing and Gigs business models as well as sharing best practices and information. More specifically the taskforce is identifying challenges and opportunities, defining potential interventions to address issues, and defining a unified national pitch for the sector. Overall, the objectives of the FROG taskforce are to enable and strengthen linkages between the elements of Freelancing, Outsourcing and Gig Economy, make FROG a sector recognized by the Ethiopian Government as a strategic pillar of economic reform, leverage the power of digital to leapfrog conventional FROG maturity stages, attract global demand to accelerate FROG job creation and increase maturity of ecosystem, and harvest local economic expansion in all sectors to fuel growth of FROG jobs. Ethiopia as an Offshoring Destination and the Emerging Outsourcing industry As part of their rightshoring strategies, Fortune 500's and multinationals have developed a knee-jerk reaction relocating their middle and back-office processes to India, the Philippines, Eastern Europe, North Africa and Central America. But as labor cost continues to rise in those parts of the world, some African countries are emerging as alternative destinations, especially due to labor arbitrage and the high availability of trainable talent. Ethiopia is the second most populous nation in Africa, with more than two hundred thousand students graduating each year with a STEM degree. Talent cost is on average fifteen times cheaper when compared to western countries, and very competitive when even compared to South Africa. For Ethiopia, positioning the country as an offshoring destination for multinationals as well as developing the local outsourcing industry could have a tremendous impact on the GDP. If on average, an Ethiopia-based company charges $15 USD for every employee in its call center, offshore development center and the like – which is still a very competitive rate compared to conventional offshoring destination – the revenue collected for every 5000 employees amounts to $150 million USD per year. This would represent significant tax income for the country in hard currency. A similar effect could be had by attracting global freelancing demand through digital platforms. [1] 2018 Ethiopian Central Statistical Agency estimates [2] Mastercard, September 2020, The Gig Economy in East Africa White-Paper  AUTHOR: Bernard Laurendeau (Managing Partner, Laurendeau & Associates) As part of their rightshoring strategies, Fortune 500's and multinationals have developed a knee-jerk reaction relocating their middle and back office processes to India, the Philippines, Eastern Europe, North Africa and Central America. But as labor cost continues to rise in those parts of the world, some African countries are emerging as alternative destinations, especially due to labor arbitrage and the high availability of trainable talent. Ethiopia is the second most populous nation in Africa, with more than two hundred thousand students graduating each year with a STEM degree. Talent cost is on average fifteen times cheaper when compared to western countries, and very competitive when even compared to South Africa. You will find more details in the Offshoring to Ethiopia factsheet we developed in partnership with Briter Bridges (www.briterbridges.com) More resources: Tech IT and BPO Directory, NTF V Ethiopia  |

RSS Feed

RSS Feed